In the realm of cars, taxes, and regulations, the status of a vehicle often takes center stage. The choice between a new or used car can have significant implications for both VAT (Value Added Tax) and BPM (Tax on Passenger Cars and Motorcycles). Let's dissect this intricate dance of fiscal intricacies.

New for VAT: A matter of time and kilometers

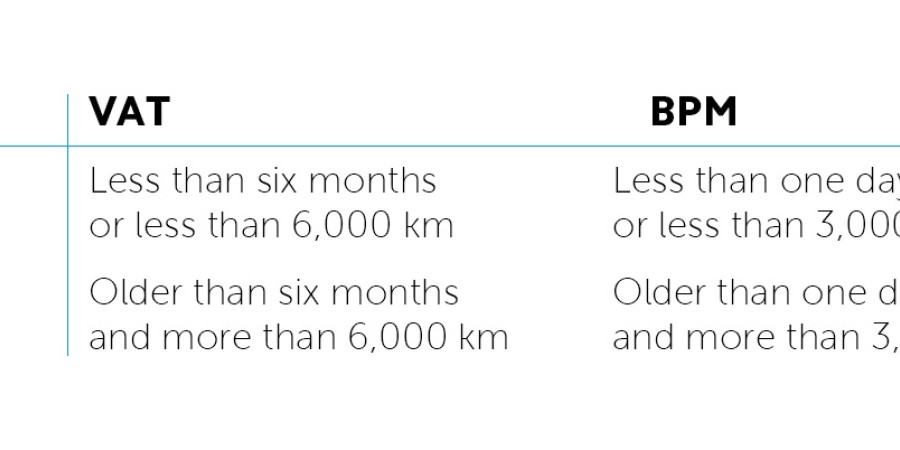

A car is considered new for VAT if it is younger than 6 months or has driven less than 6,000 kilometers. This means that even a 4-month-old car with 10,000 kilometers is deemed new for VAT. For businesses, this nuance is less relevant as they can purchase the car excluding VAT through intra-community delivery within Europe. However, for margin cars and private purchases, an additional 21% VAT applies in the Netherlands.

It's important to note that this European regulation applies in all EU countries. Keep in mind that the six-month rule pertains to the invoice date after the first registration date, not the BPM declaration date. Waiting for the car to be 6 months old for BPM declaration when the invoice has already been issued is therefore futile.

New for BPM: Unused and low mileage

For the BPM, a car is considered new if it is unused and/or has very few kilometers on the odometer. The issuance of a foreign registration certificate is not relevant in this context. For example, a car with only 10 kilometers on the odometer and a date of first registration a year earlier is considered 'fiscally new,' requiring payment of the gross BPM from the year of BPM declaration.

Used for BPM: Kilometers and substantiation

A car is deemed used for the BPM if it has demonstrably been used on the road. This implies that the car has clearly covered kilometers. A registered registration certificate serves as a solid substantiation of the used state, along with the documented mileage. Additionally, a maintenance history can also serve as evidence of usage, even without official registration. In essence, the car must have genuinely been used for its intended purpose.

The threshold for the number of driven kilometers to classify a car as used is determined by jurisprudence and court rulings. Currently, around 3,000 kilometers is considered the minimum number of kilometers to classify a car as used for the BPM. This mileage, combined with the date of first registration, designates the car as used, regardless of how recent that registration may be.

In the intricate world of taxes and cars, understanding these subtleties is crucial to avoiding unnecessary costs and confusion. Whether you opt for new or used, the financial ballet of car ownership always brings its own set of rules and requirements.

Want to learn more? Contact us for non-binding advice at import@vdsautomotive.com or by using the contact form.